Interest rates grab most of the headlines lately, but the Fed is also engaging in some behind the scenes activity as another means to slow the economy to help fight inflation. It’s also something they should have begun over a year and are only now starting to do in any meaningful way. But I digress…

What I’m referring to is called quantitative tightening or “QT”.

QT is the process the Fed is using to reduce the size of its balance sheet, which reached nearly $9 trillion at its peak earlier this year. It gets more complicated but let’s see if we can unpack some of the main mechanics of QT and how it might impact the stock market going forward.

This is the process of allowing bonds that the Fed holds on its balance sheet to mature without replacing the full amount. When a bond matures off the balance sheet and isn’t replaced, it reduces the amount of reserves in the banking system by an equal amount.

It does this by “paying back” the maturing bond by subtracting the sum from the cash balance the Treasury keeps on deposit with the Fed, effectively making the money disappear.

The idea is to tighten the availability of money, which should raise borrowing costs and slow economic growth.

Given that quantitative easing or “QE” helped form the economic recovery and provided a lift for the stock market, as well as other so-called risk assets, it seems quantitative tightening could have the opposite effect.

The Fed started the QT process in June, capping the decline at $30 billion in Treasuries and $17.5 billion per month in agency mortgage-backed securities (MBS). In October, those caps doubled to a maximum of $60 billion per month for Treasuries and $35 billion for MBS.

There’s no set time frame or target level for the balance sheet reduction, however, Fed officials have indicated a preference for holding only treasuries at a level close to 20% of gross domestic product (GDP) compared to the recent peak of about 35% of GDP. That could take some time and involve a reduction of approximately $3 to $4 trillion dollars, which would likely be spread out over several years.

Let’s dig a little deeper and try to explain why these operations have an impact on the stock market.

The liquidity created from QE and fiscal stimulus was so great that commercial banks no longer wanted deposits from large institutional clients because there were not enough safe assets available to purchase.

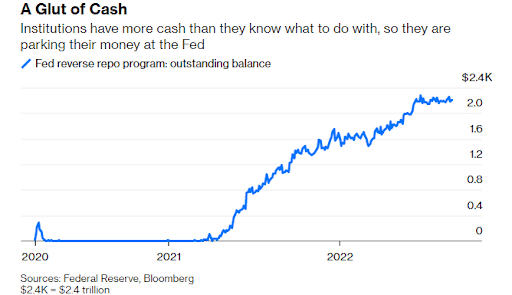

Instead, they began parking the money with the Federal Reserve in a process known as repo and reverse repurchases (RRP). The repos consist of the Fed delivering high-quality collateral with the promise to buy it back in a certain number of days at a higher price. Essentially guarantees a small profit which was higher than a 30-day T-bill would earn.

Usually, the Fed would only engage in repo operations with primary dealers, but the need to soak up extra liquidity was so great that it widened the list of eligible counter-parties to include mutual funds and other non-traditional accounts.

The overabundance of liquidity is evident from the reverse repo operation’s growth to its present $2.18 trillion size from virtually nothing before the pandemic.

Now, with rates rising there are other alternatives – T-bills went from 0.5% six months ago to a current 3.1% – and with the Fed letting bonds mature, we should see an unwinding of the balance sheet.

How this will end up impacting the stock market is unknown. We are again dealing with another “unprecedented” situation…

Continue reading at WEALTHPOP.com